#3 Risk Modeling in Post-Pandemic World ; Walking the Himalayas!

#3 Risk Modeling in Post-Pandemic World ; Walking the Himalayas!

In case, we haven’t met or don’t know each other , here is a quick bio : I am Vipul Mangla, and I have spent most of my last decade as a Management Consultant for the big spiders and wolves of our world (acronym for Banks) and in my spare time, I remain glued to content ranging from Travel to History to Psychology to Finance, basically whatever satiates my curiosity. The serving modes typically are Books, Podcasts, Webinars, OTT, Audible, Medium and other myriad links on the web.

I am known for occasionally ranting about all this content in my inner circle and this newsletter is my humble attempt to extract key learnings from this daily consumption across screens and distribute the same to a wider audience. I hope you will enjoy it and find something useful and worth your precious time !

If you like reading the content here, please do share amongst your network.

Post # 3

(You may check out the first and second posts, if you haven’t already)

What I learnt at Work : #WorkTime

I am currently working in the Global Risk Management division of Northern Trust. Risk Management in a bank entails wide variety of functions like Market Risk, Credit Risk, Operational Risk, Liquidity Risk, Cyber-security, Earning Risk, Business Resiliency, among other things. However, one of the bedrock of the Risk Management function has been Risk Analytics and Statistical Modeling, which has evolved by leaps and bounds following the aftermath of Global Financial Crisis of 2008-09.

For the uninitiated, Statistical Modeling in the risk world generally involves using the historical data (Financial Ratios, Customer information, Collateral Data, Loan Contracts, Trading and Macroeconomic Data, etc.) to predict the likelihood of a future event which can be a default by the customer, or any operational failure in a banking process, or the trading positions in the stock markets and many similar such future outcomes. This helps the bank shore up capital and keep a check on its strategy and the processes to help deal with future uncertainties.

COVID-19 crisis certainly challenged the use of established, well-developed models to evaluate rapid changes in the credit environment and their ability to provide adequate risk measures. But then , Albert Einstein said, “in the midst of every crisis, lies great opportunity.” Looking back at the post-pandemic responses by Risk Managers at various banks, I lay out three key things, which, in my opinion, can enhance the existing Risk Modeling practices and are surely here to stay.

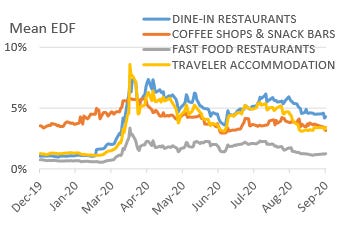

Credit Risk Segments : The traditional credit risk models segment borrowers into several broad sectors or buckets (It is very similar to the Categorical Thinking concept we talked about in the last post). However, the key theme that arose out of the crisis was the diverse behavior of different players even within the same credit segment. For example, the impact of the crisis on Accommo-dation establishments and Dine-in restaurants was quite adverse as compared to Fast Food chains/Cloud kitchens as the latter were able to leverage the food delivery ecosystem and also deploy certain socially distanced measures.

Mean EDF represents expected default frequency which provides the measure of the probability that a firm will default over a specified period of time. Source: Moody’s Analytics (Country : United States) This certainly indicates a need to rethink our existing credit segments and the level of its granularity, based on possible disruptions caused by tail events, resiliency to absorb such shocks, possible impact of sociological reaction to crisis and the level of adaptability. A similar granular analysis can be done for various other credit segments like Geography & Demographics (Country, State, District level), Business units, Customer types and banking products.

Use of Alternative Data : Another significant component of any credit risk model is the historical data input. This is mostly composed of certain macroeconomic variables like GDP, Unemployment Rate, Housing Price Index, Stock Market Indices and/or customer and loan specific components like Customer Ratings, Age of the loan, Amount of loan, Quality of collateral etc. The models help in establishing a relationship between these input variables and the outputs. For Example, a high unemployment rate generally is attributed to the increase in likelihood of default and hence, a rise in credit losses. However, the momentous support that came as a post-pandemic response from central banks challenged these relationships and previous assumptions. Risk Managers could not just rely on model outputs to calculate their expected credit loss and allowances and had to look at alternative data sources. Over the course of this year, banks have utilized many novel sources to gain insights about customer behavior, revenue streams and the possibility of loan paybacks. These range from table reservation data at Open Table to Satellite imagery of Shopping mall parking lots to scraping data from service calls to bank customer care centers for moratorium related queries and multiple other new variables.

Alternative Data sources is one key trend that would certainly gain precedence in the Risk Analytics and Modeling space, going forward.

CreditVidya - a leading Fintech player in the alternative credit scoring recently successfully patented their NLP and AI-based framework - “FeatGen” which takes into consideration 10,000+ digital data points on each borrower to underwrite loans, especially for the data starved community of under-served people across the world.

As bigger players also move towards harnessing alternative data sources more and more, issues of data integrity and data security that exist in a lot of such data sources, will also begin to streamline.

Nowcasting : Another crucial innovation has been the monitoring of world economics in real time. The fancy term for this is - ‘Nowcasting’. Nowcasting is the dynamic process of estimating economic variables that are otherwise provided infrequently and after long delays such as GDP. The delays actually mean that the estimates pertain to recent past rather than present or future. Although, this methodology is more in use for assessing the asset price fluctuations, but it can certainly evolve to lend credence to credit risk loss estimations and make it more real time. In case, anyone is interested to know more about the Dynamic Factor Model used for Nowcasting, here is an interesting article laying out Bank of England’s approach.

Every crisis is an opportunity to make the system more robust, more innovative and taking a step further to improve the firm’s efficiency ratio. Tail events surely will challenge the status quo and existing systems, but it may not necessarily mean that we need to reinvent the wheel.

As John.C.Bogle said - “Reversion to the mean is the iron rule of the financial markets.” Sometimes, it may stray off its path for longer period, but eventually it will revert back to its mean.

What I learnt at OTT : #BingeTime

Walking the Himalayas : Discovery Plus

The fun element associated with all the major UPI apps is the scratch coupon that reveals itself once you are done with any payment. This week when I completed a payment on Google Pay and rubbed my thumb over the coupon, a discounted discovery plus membership showed up. Like any middle class Indian, I am also a sucker for free stuff and when it is about exploration/travel related content, it was hard not to succumb to the freebies on offer. So, I downloaded the Discovery Plus app, mirrored the screen onto my smart TV and started exploring. Being a big travel fanatic and an ardent lover of mountains, it was quite an easy decision to begin my OTT journey for D+ with the series - ‘Walking the Himalayas’ by Levison Wood.

It is a series of grit, endurance, strength, stamina, friendship and above all, determination. Levison walks for 1700 miles across 5 countries in a span of 6 months, mingling with the locals, surviving treacherous terrain and biting cold, offering us breathtaking views of the greatest mountain range and if that is not enough, he even survives a deadly car crash and returns to continue his journey with a broken arm but an unbroken spirit. I binge watched the entire 5 episode series in one go and had almost started my research on flights to Dehradun/Srinagar/Sikkim. (MakeMyTrip flashing the ‘travel safe’ sign brought me to reality. #damncoronavirus)

Sherlocked!

I am a big fan of the Netflix series - ‘Black Mirror’. It is a dystopian science fiction anthology series examining our lives in regards to the impending consequences of the technological advancements. One of the episode in the series - ‘Be Right Back’ talks about continuing the relationship with deceased even after their death. Don’t worry, we are not there yet, but we are surely moving at a rapid pace towards it.

You would have probably heard about Deepfakes. Well, now we can have entirely new fictional persons built solely by AI algorithms and they are quite real. Hell, there are now firms selling fake people. But before technology starts deceiving us, let’s put on our sherlock hats and learn a few tricks to save us from that deception. Check out this article -No, actually ‘experience’ this article by New York Times - Designed to Deceive!

Even if you don’t want to read, do scroll through it. It is certainly an adventure in itself and you will also then have few important tricks up your sleeve at spotting ‘fake real’ people.

So, that’s it folks for this week. I hope the content was enriching and enjoyable. If you liked it, please hit the ‘Like ❤ ‘ button at the top.

Next week, we will continue our journey in the Stanford course on Human Behavior, along with some other interesting tidbits from the world of Books and Binge.

P.S: I would love to hear from you, so please drop a note with your feedback (The Good, the Bad, The Ugly) or just to say 'Hi' at vipulmangla89@gmail.com